%20(1).png?width=200&height=85&name=logo%20(1)%20(1).png)

%20(3).png?width=200&height=85&name=logo%20(1)%20(3).png)

.png?width=200&height=85&name=Group%2031%20(1).png)

%20(4).png?width=200&height=85&name=logo%20(1)%20(4).png)

.png?width=200&height=85&name=Group%2031%20(2).png)

.gif?width=1080&height=1080&name=Untitled%20design%20(2).gif "Untitled design (2)")

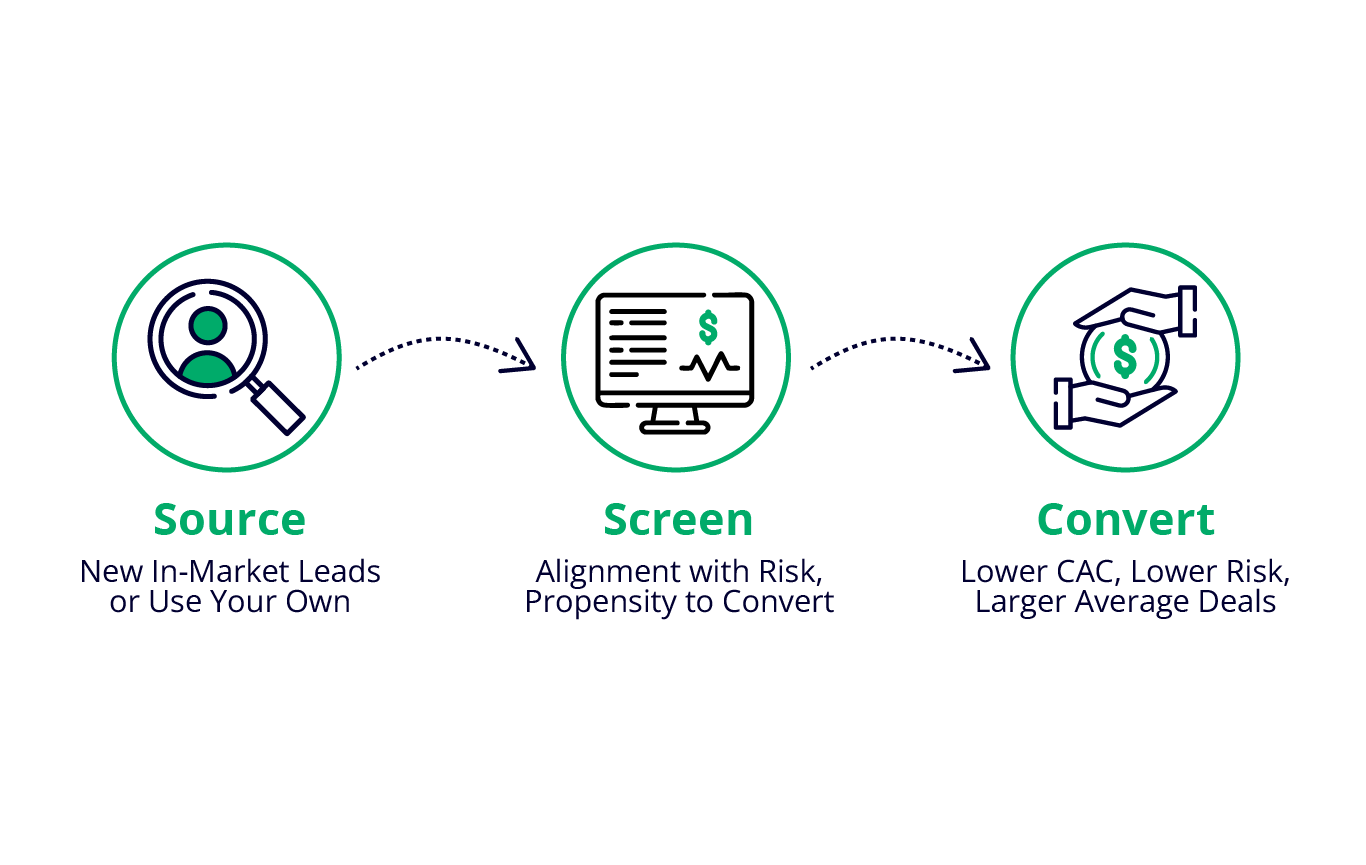

Start Approving More Borrowers, Without Increasing Risk

From powerful credit insights to real-time risk assessment tools, our products are designed to help lenders make smarter, faster, and safer lending decisions. Approve more borrowers with confidence, streamline your processes, and safeguard your portfolio with Trust Science by your side.