A large BHPH auto dealer was challenged, in the midst of an uncertain COVID-19 credit market, with approving more borrowers for financing while keeping defaults steady. Despite rapid evolution in the credit market, over 65 million Americans remain excluded from traditional credit opportunities due to a lack of credit history or access to traditional financial services: roughly 1 in 5 people are credit invisibles out of the view of the traditional credit bureaus. Regardless, this BHPH auto dealer, like others, was able to sift “prime” borrowers out of a pool of wrongly-scored “subprime” borrowers to increase good loan origination, seeing results of up to 200X ROI and an 18.8% increase in earnings over a two-year period after implementation.

“Trust Science® and its Credit Bureau +™ service exceeded my expectations and continues to do so. The service properly and accurately scores consumers who are very hard to score.”

Mark Eleoff – CEO – Eden Park

According to Credit Infocentre, a traditional credit score, as determined by the three primary credit scoring bureaus in the United States, is usually determined strictly by a borrower’s line of credit. These bureaus will look at a limited set of information, including payment history, amounts owed, length of credit history, new credit, and credit mix, to determine a score typically between 300 and 850. These criteria are not only incredibly limited in insight, but are also restrictive and exclusionary to the millions of underbanked and financially stressed Americans seeking to develop their credit. As a result, traditional credit bureaus are unable to generate an accurate credit score for approximately 53% of Americans while labelling over 50% of Americans as less-than-ideal borrowers.

Due to the limited competition in this space, lenders have become over-reliant on antiquated and rigid data and scoring systems, facing barriers in the fair and ethical scoring of specific groups of creditworthy prospects, such as immigrants and millennials. Put simply, traditional credit scoring offers rigid and limited insight to lenders an inadequate assessment of significant sectors of creditworthy prospective borrowers.

Trust Science® collaborates closely with clients in development and integration, providing significant and demonstrated improvements in lift, stability, bad loan analysis, and return on investment. By replacing the customer’s custom score with

the Six°Score™ platform, Trust Science was able to provide significant value-add and help the customer produce the following returns:

– 19.1x ROI*

– An 18.8% increase in earnings over a two-year period

– A further projected 9.5% increase in earnings in the subsequent year at 19.1x ROI on similar application volume

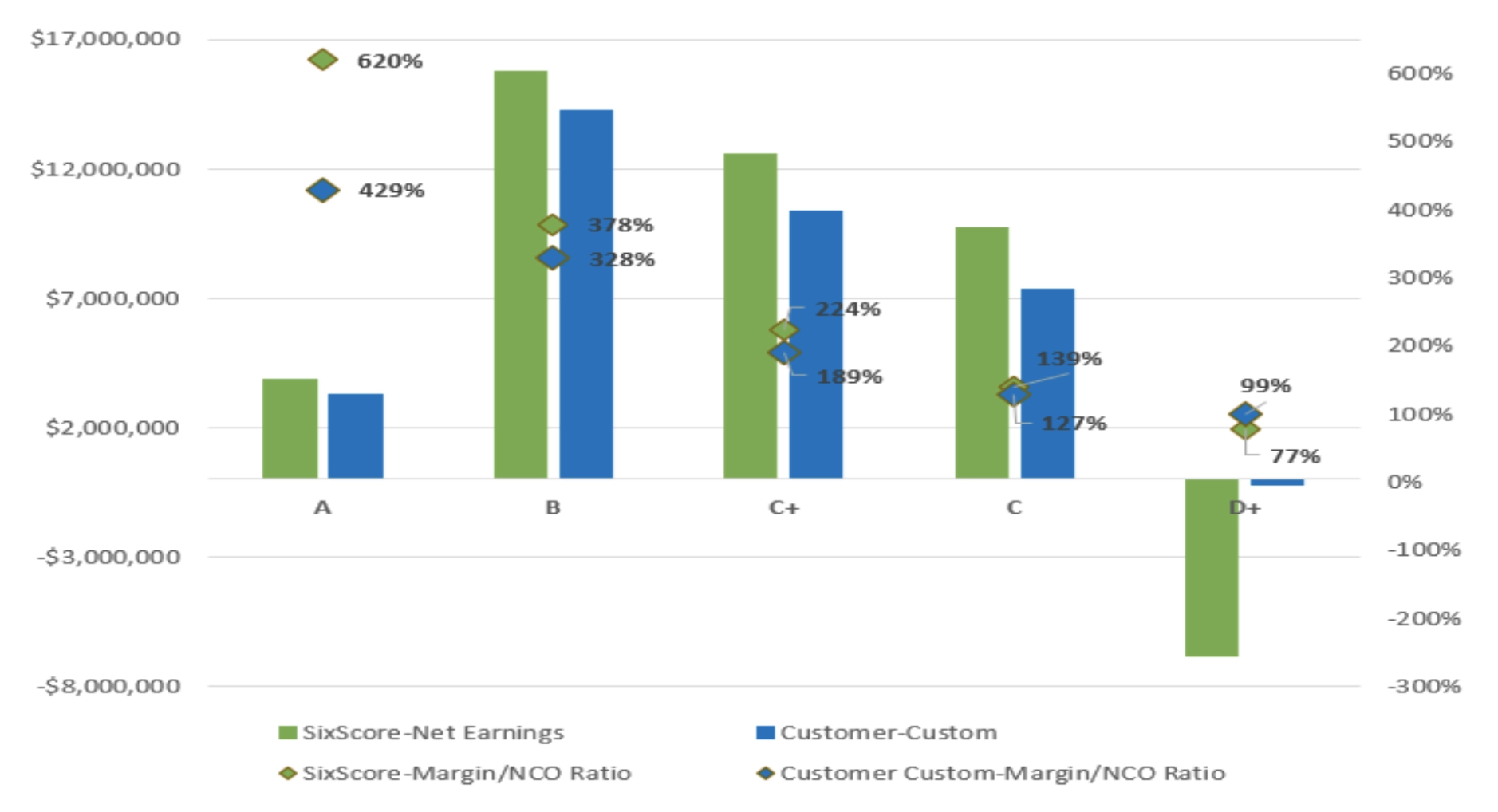

According to the results of the stability analysis performed using Trust Science’s Six°Score™, the custom Six°Score™ had a 36.9% lift on the Kolmogorov–Smirnov test and 11.3% lift on bad capture (at approximately 20% of booked loans) versus the current custom scores.

The custom Six°Score™ built by Trust Science® was able to identify bad loans better than the current customer’s custom score. It also excelled at capturing past due amounts and bad loan principal. This is demonstrated through the fact that Six°Score captured more bad loans at lower score ranges, with a maximum of 4.1% (an 8.3% lift) more bad loans in the bottom 45% of booked loans. Additionally, where Six°Score™ agreed or scored the consumer higher, the performance was better than average. Conversely, where Six°Score™ scored the consumer lower, the performance was lower than average.

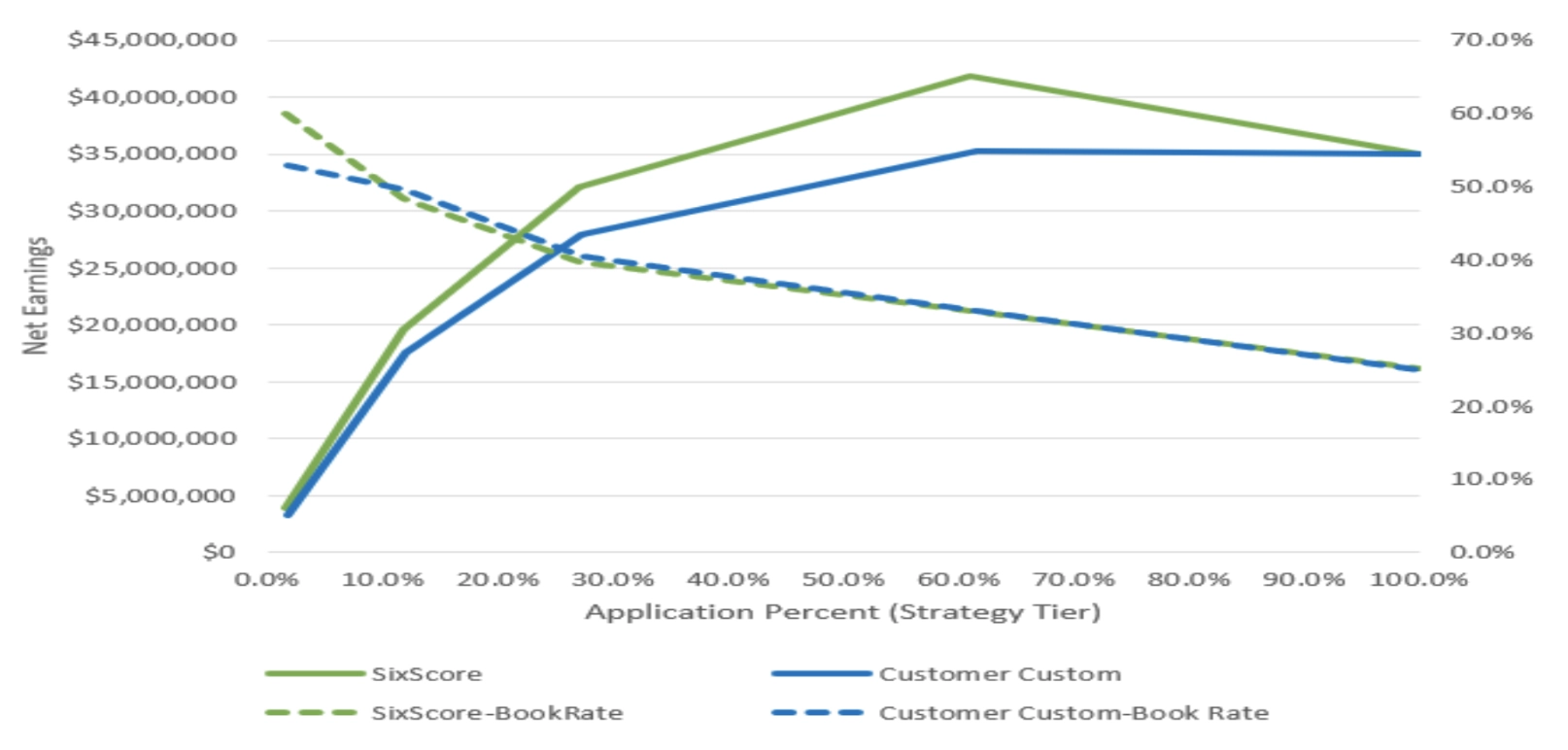

Below are some visualizations that demonstrate the performance of Trust Science’s Six°Score™ model vs. the customer’s custom score:

With this model, a more refined tier structure can be achieved with confidence. Trust Science® discovered that tier assignment based on the custom Six°Score™ tends to be lower than what was done using the customer’s custom score. The results demonstrate that the current custom score should be replaced by Six°Score™ in the customer’s underwriting strategy to achieve better business results.

By replacing the customers’ current score with Six°Score™, the customer was able to see the following results:

– An 18.8% increase in earnings over the two-year period

– A 19.1x ROI* using the current strategy

– A further projected 9.5% increase in earnings in the subsequent year at 19.1x ROI on similar application volume

By using Credit Bureau +™ by Trust Science® and Six°Score™, this BHPH dealer was able to lend to more people with confidence in their ability to avoid defaults, witnessing substantial earnings growth and ROI quickly after implementation. Trust Science® is an industry leader in its ability to use AI/ML models that grow with your business, harnessing its numerous data sources to deliver meaningful, explainable, and fully compliant risk scores, even on those that were conventionally thought of as credit invisibles.

Trust Science® is a member of the American Financial Services Association (AFSA), the Canadian Lenders Association (CLA), the National Automotive Finance Association (NAF), The Online Lenders Alliance (OLA) and the Texas Consumer Finance Association (TCFA).

Trust Science® is committed to Fair Credit Reporting Act (FCRA) compliance and helping you protect and understand your consumer profile. For more information, please see our Consumer Disclosure Page.

Trust Science®, Credit Bureau 2.0® and Troo® are trademarks that are legally registered to www.TrustScience.com Inc. by the U.S. Patent & Trademark Office.

Credit Bureau+™, Six°Score™, Smart Consent™, Hidden Prime™, Invisible Prime™, Credit Bureau 3.0™, Credit Bureau 4.0™, Personal Credit Bureau™, Personal Data Vault™, Auto Six°Score™, Auto Bureau™, Auto Credit Bureau™, Rating Agency 2.0™, Cashflow Bureau™, One Touch Lending™, Lead to Loan™, Lender in the Cloud™, Fl°wbuilder™, Fl°wbuilder™, FCRA-Compliant Insights From Lead to Loan™, Go Beyond the Bureau™, Fixing the Credit Catch-22™, Find Invisible Primes™, and Helping Lenders Find Great Borrowers™ are trademarks of www.TrustScience.com Inc.